Inflation

Each year, the Reserve Bank of Australia releases more money into circulation, but because the total combined amount of money has the same value, each dollar is now worth less to make up for the extra dollars in circulation. This devaluing of the dollar is called inflation.

Remember back when milk was $1, and now it is more than double that? It is not that milk is more expensive. It’s that each dollar is worth less, so you need more dollars to buy an item of the same value.

The number of dollars is called the nominal value, while the after-inflation value is called the real value. When the nominal value remains the same, the real value has actually gone down. Even though you have the same number of dollars, you have lost purchasing power. The loss in value over a year or two isn’t much of an issue, but at a 3% inflation rate, it takes about 20 years for your money to halve in value.

So just to maintain the real value of money, we’re going to have to find something that has a higher return than leaving it in a bank account. But before we think about living off our investments, we need to grow our assets.

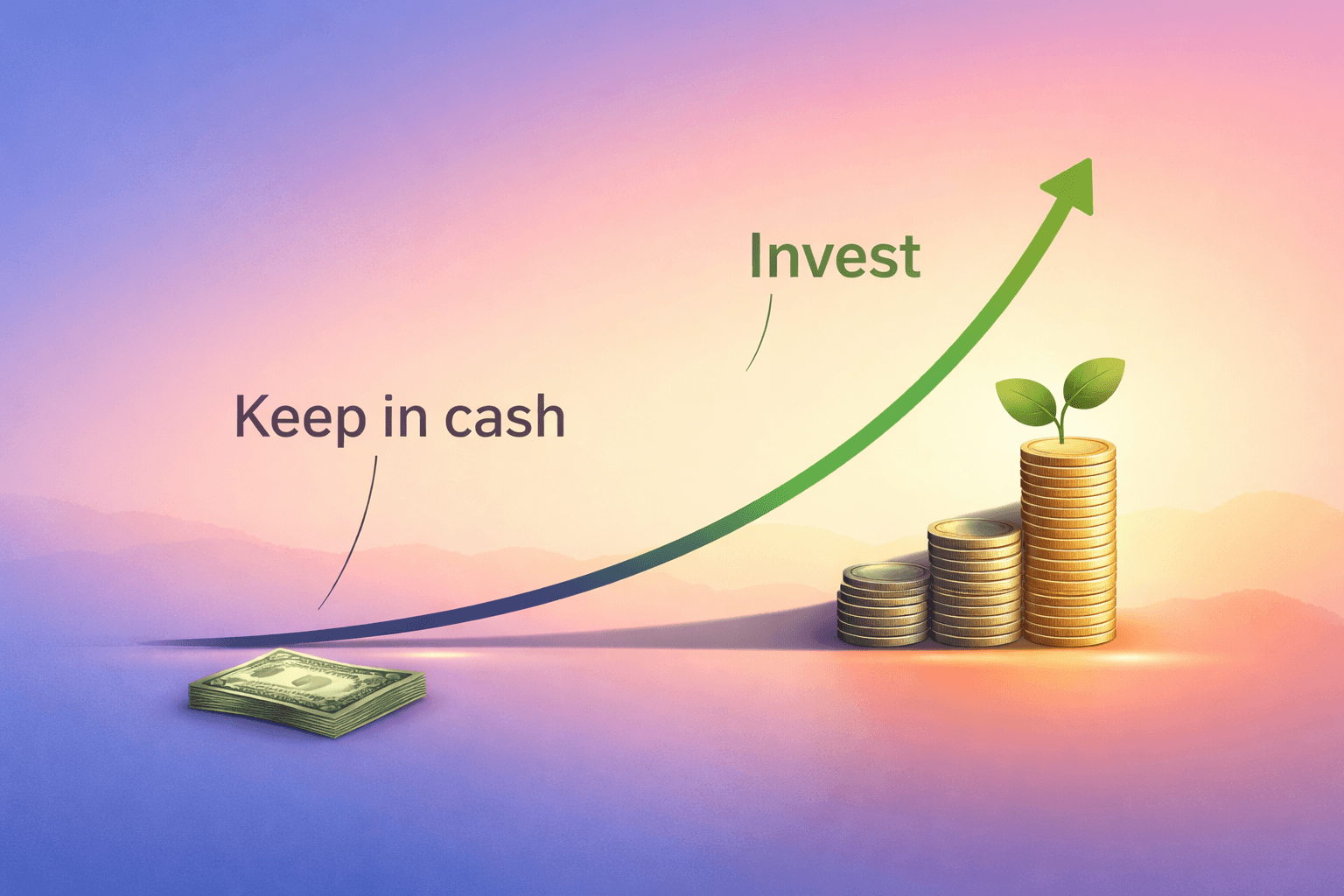

It takes many more years of working and saving to grow your assets without investing

If you were to save $20,000 a year and keep it in a bank account reinvesting interest that is equivalent to the inflation rate, after 40 years you would have $800,000 (in today’s buying power). You could expect to live off about 3.3% p.a. (assuming a 30-year retirement), which is $26,600 per year. Not a great result after 4 decades of sacrificing and saving a significant portion of your income.

If you invested it into a broadly diversified basket of stocks returning the historical average of 6% over inflation, after 40 years you would have $3,095,239. You could expect to live off about 4% p.a. (a higher percent since it generates a return even in retirement), so $120,000 per year – almost 5 times as much.

Not only does this mean you can spend more in retirement, but it also means you don’t have to work as long. If you are happy to live on $80,000 per year generated from your investments, you could retire several years earlier and still be living on three times as much as what you could if you put all your retirement savings into cash. Or you could switch to part-time after 30 years of working and saving, and spend more time with your family and on your hobbies.

If investing is so good, why doesn’t everyone do it?

Because investing comes with short-term uncertainty. It is entirely normal, and you should expect to lose money in some years. This doesn’t make it a bad idea to invest. It means it is a bad idea to invest if you need the money in the next few years and cannot leave it invested through downturns until it recovers to achieve the long-term average return. If you are saving for something you will need in the next few years, such as a car, a house deposit, or a vacation, you should not invest that money, as it could result in a permanent loss when you need it.

However, saving only in cash won’t work. If we’re going to live off our investments for decades, we’re going to have to find something with a higher return.