I had a reader ask:

I’d like to know why you avoid VISM (small caps)? Is it necessary to include VISM for total world exposure? Why are small caps considered risky?

There’s nothing wrong with small caps. The reasons why I haven’t discussed them on this site until now are:

- The goal of this website is to give the most valuable 5% of information that provides 95% of investing success.

- There’s conflicting research on the benefit of small caps.

- Any higher returns are not a free lunch – they come at the cost of higher risk.

Conflicting research

Initially, the research found that small caps provided higher returns, even when accounting for risk, which made them very lucrative because if this was true, you could replace large caps with a combination of small caps and enough bonds to dial down the risk back to that of large caps, and you have a higher return with no more risk! Who doesn’t like free money?

Unfortunately, that research was later re-done and with more data, and it was found that small cap growth companies dragged down a lot of the broader small cap market return. So there is no free lunch after all.

What is ‘growth’ when talking about ‘small cap growth companies’? Well, just as you can separate companies into small, mid, and large, you can also slice them into another dimension of value, blend, and growth.

Value companies are those that are valued at low levels relative to tangible metrics such as earnings and book value. Generally, these are undervalued for a reason – either the industry or sector is suffering, the country itself is suffering economically, or it could be due to the company itself being poorly run. Growth companies, on the other hand, are those that appear to have a bright future. People see it and are willing to pay more than their fundamental tangible measurements, such as earnings and book value, in the belief they will grow and meet those expectations later (think tech companies as a current example). Small growth companies are sometimes called lottery companies because they sometimes shoot the lights out and grow enormously (think 10x or more), but most of the time they don’t make it, and as a whole they’ve been the worst-performing segment. You can see why they are called lottery companies!

Here is more information on small caps and their conflicting research.

The Problem With Small Cap Stocks – Ben Felix

Small Cap Blend vs Small Cap Value – Bogleheads.org

Telling Tales – 2017 update – Siamond – Bogleheads.org

Fresh Look at the “Larry Portfolio” from Portfolio Charts – Bogleheads.org

Why are small caps considered risky?

Large companies can afford to throw massive amounts of money at problems to overcome them. Small companies don’t have this ability. As a result, the smaller the company, the less likely they are to survive. We see successful large companies and are aware that they began as small companies, but often forget that the overwhelming majority of those small businesses failed or were taken over. Buyers of shares are aware of this, and as a result, they price-in the higher risk by way of not being willing to pay as much, thereby ensuring that if the company goes under, they lose less money on average. Not only to avoid losing more ‘on average’ when accounting for the higher number of failures, but even more to compensate for this higher risk (otherwise there would be no point in taking on higher risk by buying those shares if not for a higher return commensurate with it). More on risk premium here.

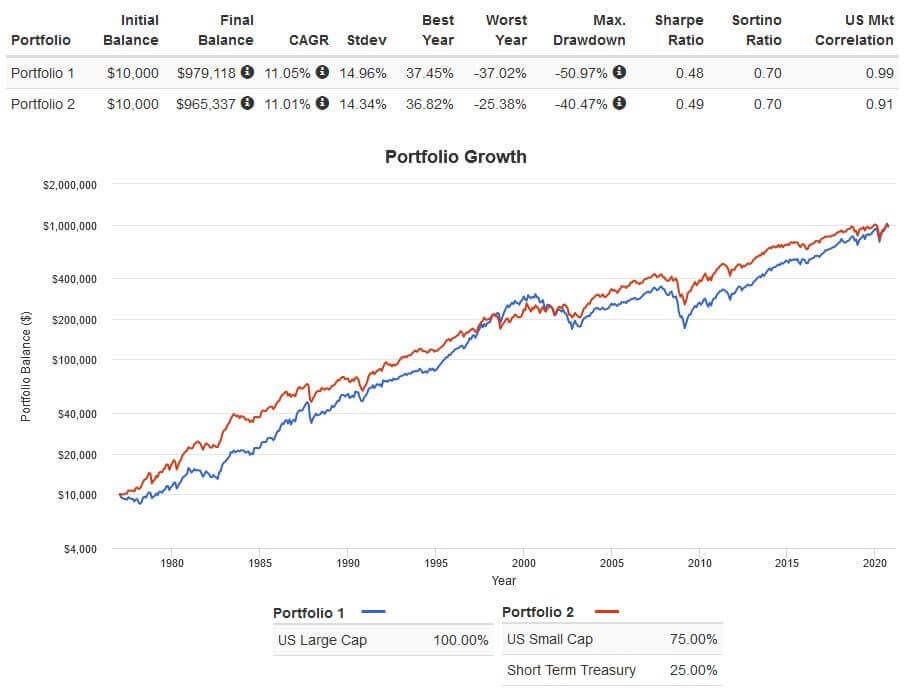

So, while the higher risk can be useful in that you get a higher expected return, that higher return comes at the cost of more risk. Below is a comparison of a 100% US large-cap allocation to an allocation of 75% small caps and 25% short term treasuries. It shows that both the risk (stdev) and return (CAGR) are virtually identical, so there is no free lunch with small caps. You are simply increasing your risk, similar to just having a higher stock-to-bond ratio.

Having said that, once your equity allocation reaches 100%, adding small caps is one way to add further risk for an increased expected return without the added complications of adding leverage.

Source www.portfoliovisualizer.com

An alternative for increasing risk

If you already have a 100% equities portfolio and have a very high risk tolerance, then adding some small caps could increase the risk and return of your portfolio.

The downside of this is that large-cap and mid-cap companies make up 85% of the investable market by capitalisation for a reason – they are well-established, generally profitable, and have a lot of money to throw at problems, so their risk is typically lower than that of small-cap companies. You probably would not want to have an overwhelming amount of your portfolio in small cap companies for this reason, and if you had, say, 15-20%, then your total portfolio level of risk and return isn’t all that much different.

As of 2024, there is another option to increase your risk and expected return – an internally leveraged ETF, GHHF.

GHHF is a leveraged ETF with an asset allocation similar to DHHF (Betashares all-in-one all-growth ETF), but it differs from most leveraged ETFs in that it is moderately leveraged, infrequently rebalanced, and has lower management fees, making it more appropriate for long-term passive investing. However, while it is appropriate for long-term passive investing, it is still further up on the risk-return spectrum than an unleveraged fund, so it is only suitable for those with a very high risk tolerance. Read more about GHHF in that link.

What about small cap value?

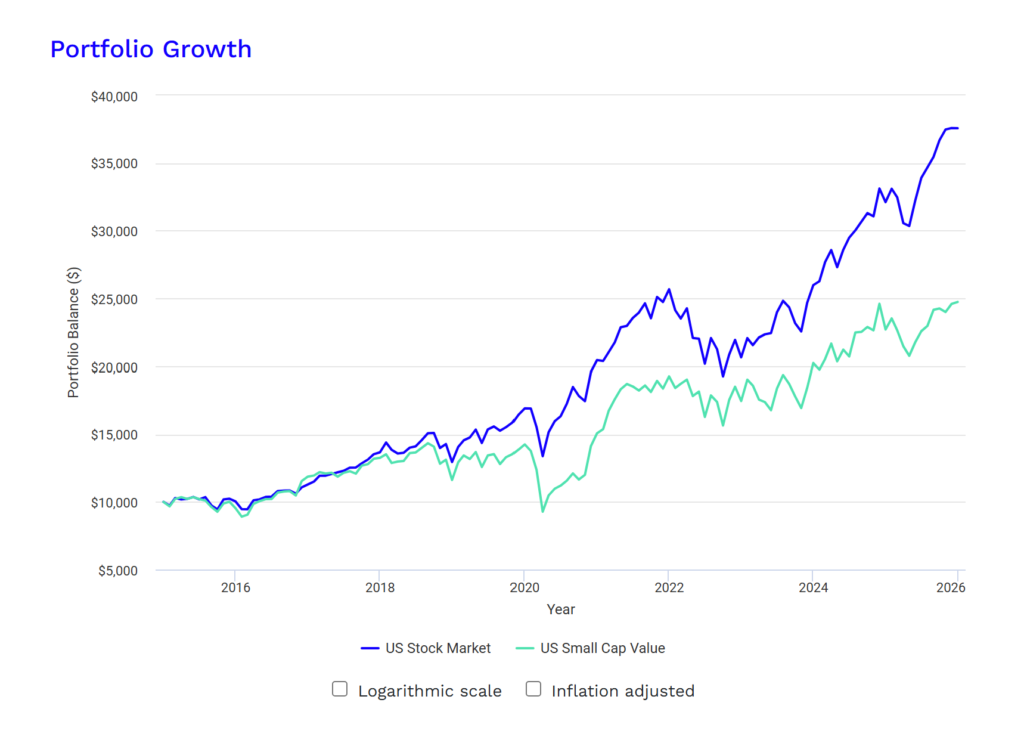

A broad market index is pure exposure to the market, but because it is cap-weighted (weighted by company market value), the largest-growth companies make up the majority of the portfolio and therefore drive most of its returns. So when we talk about the market, we’re really talking largely about the behaviour of large cap growth stocks, since they account for most of the index’s movement.

Small cap value (SCV), by contrast, deliberately shifts away from that concentration. It still has some market exposure, but it adds meaningful tilts toward smaller companies and cheaper companies – areas that are underrepresented in a cap-weighted index. These segments are influenced by different economic risks (like liquidity constraints or financial distress) and don’t move in perfect lockstep with large caps.

That’s where the diversification comes from. A market index gives you mostly large cap growth-driven market risk, while SCV introduces additional, distinct sources of risk and return that behave differently over time. You’re not just getting more of the same exposure – you’re reducing reliance on large caps and adding other compensated risks, at the cost of higher volatility and potentially long periods of underperformance.

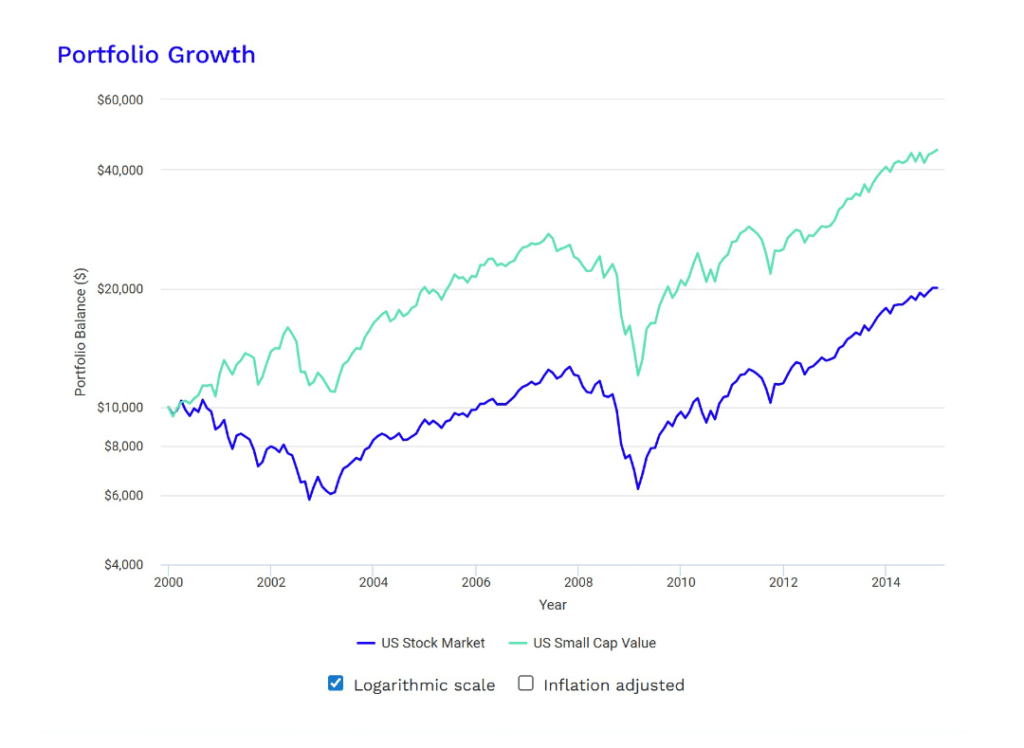

You can see an example of this diversification starting at 2000, where US large cap growth was dominated by overvalued tech companies, and the tech wreck resulted in the index falling by 45% over a long and painful three years before it turned around. In contrast, SCV fell by 31%, which meant it also recovered sooner.

This is not intended to show that small-cap value outperforms more generally. It went on to underperform for over 10 years after that, as large-cap growth stocks had a period of massive overperformance relative to their historical average, as shown below.

The point is that by adding SCV, you diversify by reducing reliance on a narrow group of large growth stocks and adding another source of potential returns across different market conditions.

Small cap value funds on the ASX

Until recently (early 2026), we didn’t have SCV funds available on the ASX. However, after many years, Avantis has finally come to Australia, and it offers AVSV (Avantis Global Small Cap Value ETF), an Australian-domiciled wrapper for its UCITS fund in Europe.

I like AVSV, and it addresses the problem of small-cap growth companies in VISM (Vanguard’s small companies fund) the problem of not targeting small companies in VVLU (Vanguard’s global value fund).

The only thing preventing me from starting to use AVSV is its very low assets under management (AUM) and the fact that it is not growing much. This is because with funds that don’t grow to $100-200m, there is a very real risk of it being closed down and investors having to realise capital gains when they pay out from the sale.

At the start of April 2026 (the time of this article’s update), they had moved from being listed on the CBOE to the ASX. I don’t know if that will help with people buying it and the fund growing to a size that is unlikely to be closed, but if it does, I like it a lot as a diversifier.

The downside of small cap value

When overweighting SCV, just as with overweighting small caps or any other segment of the market, you have to be keenly aware of how hard it is to continue holding after a decade or more of underperformance, particularly as you see people left and right telling you why it will never do well again and abandoning it.

Don’t discount the difficulty of this. I recall a few years ago, there were loads of threads on Bogleheads from people abandoning SCV after well over a decade of underperformance for this very reason. Selling it at a low point meant they would have done better by never investing in it in the first place and simply remaining in the broader index.

You need to be quite confident that it will be held no matter what before you ever decide to add this into your portfolio, which means that you need a long investment time horizon where you won’t need access to the money invested in it, and even more importantly, you plan for it to be a permanent allocation, no matter what the markets are doing.

Can I just leave out small caps and small cap value?

Short answer – yes!

There is a diversification benefit with these funds (less so with small caps). However, at some point, the number of funds you hold is going to add complexity to managing your portfolio while adding diminishing diversification benefits, and you have to draw the line somewhere. For instance, it would help diversification to replace some of the Australian index with a fund like Ex20 (which invests in the top 200 Australian companies minus the top 20 that comprise most of the index), VGE (emerging markets), you could also add some IHEB (emerging markets bonds), some DJRE (global REITs), some IFRA (global infrastructure), and you are up to managing almost 10 funds when including your base portfolio.

You have to draw the line somewhere. The simplicity of Australian equities, global equities, and global equities (AUD-hedged) are the big three. Anything beyond that is a trade-off between benefit and complexity.

If I want to include it, how much should I use?

One way is to take the global equities and apportion it into cap-weighted proportions.

Let’s say you decided on 50/50 AUD/non-AUD for currency exposure, and 25% in Australian equities.

This would give you:

50% AUD

Australian equities 25%

Developed market equities AUD-hedged 25%

50% Non-AUD

Developed market equities LC/MC

Developed market equities SC

Emerging market equities

Cap-weighting is currently:

| Developed LC/MC | 76.5% |

| Developed SC | 13.5% |

| Emerging | 10% |

Which translates to the following in your 75% global allocation:

| Developed LC/MC | 76.5% | x 75% | = 57.5% |

| Developed SC | 13.5% | x 75% | = 10% |

| Emerging | 10% | x 75% | = 7.5% |

Which comes out to:

50% AUD

Australian equities 25%

Developed market equities AUD-hedged 25%

50% Non-AUD

Developed market equities LC/MC (57.5% – 25% =) 32.5%

Developed market equities SC 10%

Emerging market equities 7.5%

Using global allocation around cap-weighting is what Vanguard and Betashares do in their all-in-one diversified funds.

Another option is to tilt toward small cap value and increase them. Just be aware that you are increasing the overall risk of your portfolio. Also, be aware that large caps and small caps can underperform for long periods. If you have a substantial allocation of small cap value, you need to be willing to hold them for a decade or more of possible underperformance. If you give up along the way, you would have done better by just leaving them out in the first place.

In reality, using 10% vs 15% won’t make an overwhelming difference. What’s more important is having an allocation that you stick to relentlessly. An allocation should be like a marriage – something you commit to permanently.

Final thoughts

As you can see, there’s no ‘right’ thing to do regarding including or excluding small caps or small cap value, and it’s a perfectly good stance to take of – why complicate education with something that is ambiguous and takes attention away from the big fundamental concepts like the risk-reward spectrum, risk tolerance, and making a plan, which in relative terms makes the decision to include a separate small cap fund barely relevant.

Having said that, there are some benefits

- Increasing risk beyond a 100% stock portfolio – although this can be achieved more efficiently with leverage

- Diversifying out of large-cap growth companies that dominate the market portfolio.