An all-in-one fund is exactly what it sounds like: a single fund that contains a complete, diversified portfolio. Instead of buying individual funds, you invest in a single fund that already holds a mix of them for you. The fund manager decides how much to allocate to each asset class and typically maintains that balance over time through automatic rebalancing.

The allocation of individual asset classes in each investment option varies with its risk profile. For instance, the higher growth options have more shares and less bonds and cash, whereas the more conservative options have less shares and more bonds and cash.

There are 5 risk profiles of all-in-one funds to choose from:

- High growth

- Growth

- Balanced

- Conservative balanced

- Conservative

Quick Links

- What high growth, high risk, and balanced means

- Considerations when choosing a diversified fund or rolling your own

- All-in-one diversified funds on the Australian market

- Final thoughts

What high growth, high risk, and balanced means

With all-in-one funds, the words “high growth” and “high risk” (and balanced and conservative) don’t have quite the same meaning as those words do in regular conversations.

In regular conversations, we think of something as risky when there is a chance of a significant and permanent loss.

In investing language, stocks are called high risk because the short- and medium-term price goes up and down so much that you have a ‘high risk’ of (potentially large) short- and medium-term loss. But in the long term, they provide a higher expected return.

On the other hand, bonds or fixed-term deposits have almost zero short- or medium-term risk since the capital is returned on maturity.

So, in the all-in-one funds, they call the funds with most or all in stocks ‘high risk‘ or ‘high growth‘, and those with most or all in bonds ‘conservative‘, and those with 50/50 ‘balanced‘.

But over the long term, bonds return much less, so even though they have less short-term volatility (i.e. what they call risk), they give you a much more significant risk of not earning enough money that you need to last the long term in retirement. Equities (another name for stocks) are risky over the short term due to market volatility, whereas bonds are risky over the long term due to lower returns and the impact of inflation. Equities provide safety against inflation over the long term, given the (historically) higher-than-inflation returns.

A high-growth or high-risk fund is simply a fund with most or all stocks and little or no bonds. So, if you already invest in VAS or VGS and little to no bonds or cash, your investment is already high risk or high growth.

But at the same time, if you don’t need to draw on your money for decades, bonds are not as important, and a ‘high risk’ portfolio with less bonds actually gives you a lower risk of ending up without enough money to last through retirement.

Stocks and bonds both have their uses because multiple competing risks need to be addressed when constructing a portfolio.

Considerations when choosing a diversified fund or rolling your own

When it comes to investing, simplicity and control sit at opposite ends of the spectrum. On one side are these all-in-one funds, packaged portfolios that bundle diversification, asset allocation, and ongoing management into a single, effortless investment. On the other side are individual component funds, where investors build their own portfolios, choosing exactly how much to allocate to each underlying asset class.

The choice between these approaches is about time, temperament, how much involvement you want in managing your money, and how much you value a “set-and-forget” solution that removes decision-making and reduces the risk of tinkering or whether you prefer the flexibility to tailor your portfolio, optimise costs, and adjust strategy as your goals evolve. This trade-off is at the heart of the decision. Understanding each aspect is key to choosing an approach that not only performs well on paper, but one you can stick with through market turbulence.

Pros of a diversified fund

1. Simplicity and ease

When you choose an all-in-one fund, there is nothing more to do. You can spend your time focusing on your career and other non-financial parts of your life, such as your family, travel, hobbies, and so on. You just take out money each month from your pay cheque and add it to your fund, and you’re done!

2. No need to rebalance

When you go the DIY route, as the values of your asset classes change over time, so does the risk-return profile of your overall portfolio. To bring it back, you need to rebalance. During small market changes, this is easy enough by always adding to the one that is most underweight, but in a bear market, when your equities (another word for stocks or shares) are falling in value before your eyes, it becomes very difficult to sell some of your safe assets and add them to your risky assets to take advantage of buying low. Having the fund do this for you becomes a more significant benefit than many realise.

3. Removes behavioural risk

The biggest risk to long-term performance is an investor changing their allocations based on what they saw on the news or heard at the water cooler. Someone will say there’s a recession coming, and you lower your proportion of Australian equities. Of course, the market so often makes fools of us and goes in the opposite direction. You sell right before Australian equities rise, resulting in a lower return than if you had left it alone, as you should have.

This is the most significant advantage of all-in-one funds – the allocations are set, and you can’t sabotage your returns by tinkering.

Nobody thinks they will mess it up and change allocations based on everyone saying which way the market will go or stop rebalancing into the falling asset class, but it is human nature to do so. For many, this alone will make it better to go with the all-in-one even at the slightly higher fee.

There are various studies on investors’ actual returns compared to the index’s returns. One I recall quoted 2-3% lower performance, and another around 1%, so if you’re a tinkerer who is always trying to find the absolute best investments, by going the DIY route, you might be saving a small amount, but paying for it with 1% lower performance is a terrible trade-off.

4. Enables your partner to manage finances when you’re unable to

One more advantage of all-in-one funds that are seldom spoken of is that one day you’re not going to be around anymore, and most likely, your partner hasn’t got a clue about how to manage a portfolio, or the interest to learn, or the ability to find the unbiased information required to learn even if they wanted to. Having a single-fund portfolio for them to draw down from will be very straightforward and will save them a lot of trouble later in figuring out what to do. Also, you may think you can just switch to that later, but there’s no reason you couldn’t get hit by a vehicle, and even if you did have time to prepare, you would face the cost of realising significant gains to switch from a multi-fund portfolio to a one-fund portfolio.

Pros of the DIY approach

1. The cost

The annual management expense ratio (MER) for these pre-mixed funds is higher than buying the individual components. The most popular funds on the market are Betashares’ all-growth ETF at 0.19% and Vanguard’s diversified funds at 0.27%. In contrast, the component funds are between 0.04% and 0.10%

To put it in context, I normally consider costs based on a $1M portfolio, so the cost is $1,900 – $2,700 per year.

If you’re willing to buy the individual funds and just top up the lowest performer each time you add funds to your portfolio, it will have an MER of under 0.10%, and for a $1M portfolio, that’s under $1,000 per year. Not insignificant, in my opinion, considering the extra work involved is a few minutes a year.

2. Ability to customise

Aspects that are worth customisation in a portfolio include:

- Growth-to-defensive (stock-to-bond) ratio

The ability to customise this would enable not needing to sell down an all-in-one that contains both stocks and bonds as your risk tolerance falls, which typically happens as you move closer to the drawdown phase of retirement. A compromise could be using a single all-growth fund combined with a bond or cash fund for your defensive assets. This would keep things simpler while maintaining flexibility around this aspect. - Home bias

You might have investment property, in which case, there is likely no need for investment in the concentrated Australian equities market at all. Conversely, if you retired young and chose to rent, a higher proportion of AUD-based equities might be more suitable.

You also may consider 40% of your equity allocation in the concentrated Australian market, which these all-in-one funds tend to have, to have more concentration risk than you consider reasonable.

The Australian stock market accounts for just 2.5% of the world’s markets by cap weight (company valuation proportions), and around half of its total value is held by just 10 companies and 2 sectors. If that isn’t enough, the value of your house, bonds, cash, and income is all tied to the Australian economy. The question is whether you want 40% of your equities tied to it as well. If there’s an isolated economic downturn, how much of your assets are you comfortable being exposed to it? - Tax efficiency

Splitting up the individual components allows you to use lower-yielding investments outside super to minimise the addition of income that is taxed at your marginal tax rate each year, while balancing that with more of your higher-yielding Australian holdings within super to improve tax efficiency while maintaining your overall target allocation. This is particularly important for those on the highest marginal tax rate, especially when negatively gearing your investments outside super by borrowing to invest or through debt recycling. - Currency exposure

This is more relevant in the drawdown phase, when stability is perhaps a bit more important, and, given the higher MER on hedged funds, it could be left until closer to retirement to add to your portfolio.

All-in-one diversified funds are inflexible when it comes to these customisations.

3. Tax efficiency

When you retire and enter the distribution phase of your investments, if you have your funds split across asset classes, you can withdraw from the outperforming asset class to bring your allocation closer to your target.

But if you have an all-in-one, you have no choice but to sell a piece of each asset class, including the underperformers. Then the fund manager will end up buying more of the same underperformer as part of their rebalancing, so you have to pay CGT on those realised gains where you otherwise wouldn’t.

This is most relevant for splitting between stocks and bonds, which have a low correlation, more than between the different equity classes.

Splitting it up also lets you keep your bond portion in your super, as bonds are tax-inefficient, which you can’t do with all-in-one diversified funds since they all include a fixed-income allocation.

You could go with a 2-fund portfolio of an all-growth fund with a separate bond fund placed in super, reducing tax inefficiency.

All-in-one diversified funds on the Australian market

These are the most commonly used all-in-one ETFs available on the Australian market.

They are placed in their order on the risk-return spectrum from most conservative to most aggressive, with the last item being a geared ETF.

| Fund | Risk Profile | AA [1] | % Aus Shares [2] |

AUD % [3] | Fees (M.E.R.) |

|---|---|---|---|---|---|

| VDCO | Conservative | 30 / 70 | 40% | 87.5% | 0.27% |

| VDBA | Balanced | 50 / 50 | 40% | 79% | 0.27% |

| VDGR | Growth | 70 / 30 | 40% | 70.5% | 0.27% |

| VDHG | High Growth | 90 / 10 | 40% | 62% | 0.27% |

| VDAL | All Growth | 100 / 0 | 40% | 58% | 0.27% |

| DHHF | All Growth | 100 / 0 | 37% | 37% | 0.19% |

| GHHF | Leveraged | 150 / -50 | 37% | 56% | 0.35% [4] |

[2] % Aus Shares = The percentage of the stocks that are Australian

[3] AUD % = The percentage of the total assets in the fund that are AUD-based

[4] Percentage of gross asset value

Now that we understand what the fund names mean and the broad information, let’s take a look under the hood.

Vanguard’s diversified funds (VDCO, VDBA, VDGR, VDHG, VDAL)

Here is a breakdown of Vanguard’s diversified funds.

| Fund | Risk Profile | Asset allocation stocks to bonds |

|---|---|---|

| VDCO | Conservative | 30 / 70 |

| VDBA | Balance | 50 / 50 |

| VDGR | Growth | 70 / 30 |

| VDHG | High Growth | 90 / 10 |

| VDAL | All Growth | 100 / 0 |

Vanguard’s diversified funds invest in over 10,000 companies in 46 countries.

If you take a look back at our previous articles on risk tolerance, equity funds and personalising your AUD to non-AUD allocation, you can see that a personalised investment allocation is as simple as answering 3 questions

- Determine your equities to fixed income allocation based on your risk tolerance.

- Determine your AUD to non-AUD asset allocation based on your total wealth and liabilities.

- Determine how much you want in Australian equities (VAS) vs global equities AUD-hedged (VGAD).

With the Vanguard diversified funds, the first question is left to your decision of which fund you chose, so we will take a look at how the next 2 are split within the diversified funds.

In all the funds, the equity portion is split the same.

They’re the managed fund versions of the following.

| VAS | 40% | |

| VGS | 29% | |

| VGAD | 18% | |

| VISM | 7% | |

| VGE | 6% |

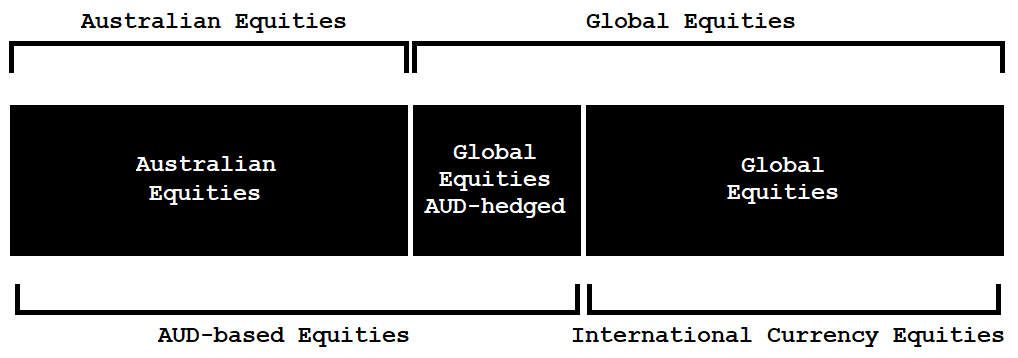

To make it more obvious, what they have is

- 40% Australian equities

- 18% Global equities AUD-hedged

- 42% Global equities

Resulting in

- Australian equities to global equities 40/60

- AUD-based equities to international currency equities 58/42

As you can see, they’ve decided on a generic allocation that is roughly what you would expect to be an average of the general population’s needs.

Regarding the allocation to Australian equities, Vanguard has similar diversified funds in Canada, but with 30% in home country equities as opposed to the 40% they decided to use in the Australian version. They’ve mentioned in research papers that franking credits have a place in determining home country equity proportion, which explains why they went for a higher portion of Australian equities (VAS).

Regarding the AUD to international currency allocation, it looks like a good average across the general population. Someone with less AUD assets outside their equities (property, bonds, cash, business) would be well-served with a bit more AUD based equities (VAS/VGAD). Someone with more AUD based assets outside their equities would be well-served with less AUD based equities, but this is a good average for someone more inclined to keep it simple.

Also, note that the total global equities (combined hedged and unhedged) is in cap-weighted proportions, which means they have maintained market-priced proportions of large, medium, and small companies in 45 developed and emerging countries – avoiding active management risk of trying to guess which asset classes will do what in the future.

Tax Drag in Vanguard’s Diversified Funds

Most of Vanguard’s funds have an ETF version and a managed fund version. Each corresponding one holds the same underlying investments, but the structure of a managed fund is far more tax inefficiency than the ETF structure as explained here: Managed funds vs ETFs

Unfortunately, the funds Vanguard used within the original diversified funds are managed funds, which are very tax-inefficient, as explained here: How is VDHG tax-inefficient?

It is worth noting that VDAL came about after this, and should not suffer from this problem. So, if you were considering VDHG (the high growth all-in-one), it may be worth considering VDAL, which is very similar, but without the 10% defensive assets, but also being much more tax efficient.

DHHF (Betashares all-in-one all-growth ETF)

Asset allocation characteristics

- 100% equities (using only total market index funds)

- 37% Australian equities (A200) and 63% global equities

- The global equities will be weighted according to the all-world-all-cap benchmark. In other words, they don’t have a static allocation to each underlying ETF – their weights will vary as the market does. This includes large, mid, and small global companies as well as emerging markets using the following US-domiciled funds:

VTI US total stock market

SPDW Developed World Ex-US

SPEM Emerging markets

37% Australian shares and no AREITs (Australian REITs)

A big improvement in diversification from BetaShares previous version of the fund, bringing the global equities up to 63% from their previous 50% (of the equities). At 37% Australian equities, it’s a bit sneaky being marginally lower than Vanguard’s 40% (of their equities), but they’re probably doing what I suspect Vanguard is also doing, which is to avoid alienating market share of individuals stuck with the outdated idea of home bias.

No AUD-hedged global equities

This seems logical. AUD-hedged global equities make sense as a replacement when lowering the proportion of Australian equities. It reduces the concentration risk of the Australian market while maintaining the AUD allocation across the whole portfolio. But Vanguard’s funds already have 40% of equities in Australian equities, and having another 18% in AUD-hedged global equities, combined with an investor’s other AUD assets (cash, bonds, house, income), seems like they may be lacking the international currency diversification that a more substantial allocation of unhedged global equities would bring.

Cost

There is tax drag in US-domiciled funds that hold non-US assets (in this case, SPDW & SPEM). Reddit user HockeyMonkey went through the PDS’s and found the tax drag to be about 9 basis points bringing the cost of MER + tax drag to 0.28%, which is basically the same as VDHG (1 basis point is immaterial).

A short summary of tax drag:

When an Australian fund holds a US fund that holds stocks from companies in non-US countries, you cannot claim the dividend withholding tax credits paid by the fund that you could claim if the Australian fund held them directly.

Here is a list of countries that Australia has a double taxation agreement (DTA) with – there are a lot of them.

Income Tax Treaties | Treasury.gov.au

Claiming tax credits means you get money back in your pocket for tax paid on your behalf, and an inability to claim that tax back results in a loss referred to as tax drag.

Besides tax drag, there’s a tax-efficient upside to DHHF over Vanguard’s funds, which is that DHHF holds ETFs within them, unlike Vanguard, which holds the non-ETF version of their funds within them.

A short summary of the tax efficiency of ETFs over managed funds:

The entire fund is one pool of assets in managed funds, so other investors selling their units triggers capital gains for all the fund’s investors. So even if you don’t sell any units, you still have to realise capital gains. This doesn’t occur with ETFs due to their tax structure, and instead, you defer these capital gains until you sell your ETF shares.

Unlike tax-drag, where money is lost due to an inability to claim the tax paid, in this case, you’re paying tax sooner.

Unfortunately, it’s impossible to quantify the cost of this because it’s dependent on how long the asset is held, but as noted here and here, it’s enough for some to avoid Vanguard’s all-in-one funds entirely and use the individual ETFs.

Vanguard is moving to change this. It will be very slow to change their existing ETFs (VDHG, VDGR, VDBA, VDCO) to avoid realising capital gains for investors, but VDAL, their new all-growth fund, is mostly made up of the underlying ETF units.

For a young accumulator with a long investment time horizon, DHHF is an excellent product to consider. It is a single fund with nothing else to do; it uses ETFs within it, making it more tax-efficient; currency hedging may not be needed for those with a very long investment time horizon; and it leaves it to the investor to add their own bonds and hedging when the time comes.

GHHF (Betashares Geared ETF)

GHHF is a leveraged ETF with an asset allocation similar to DHHF (Betashares all-in-one all-growth ETF). It differs from most leveraged ETFs in that it is moderately leveraged and has lower management fees than other leveraged ETFs, making it potentially suitable for long-term passive investing in the right situation. However, while it is appropriate for long-term passive investing, it is still further up on the risk-return spectrum than an unleveraged fund, so it is only suitable for those with a very high risk tolerance.

GHHFs gearing ratio (the total amount borrowed and expressed as a percentage of the total assets of the fund, similar to a loan-to-value ratio, or LVR) will generally vary between 30% and 40%, which means you have between 1.43 – 1.67 times the unleveraged amount (called the ‘gross asset value’). I typically think of it as roughly 1.5x.

As a result, your daily returns will be about 1.5x that of a 100% stock portfolio with a similar asset allocation, less the cost of the interest, and the ups and downs will be about 1.5x that of a 100% stock portfolio.

GHHF is suited to those who:

- Prefer an all-in-one fund over the individual components

- Are happy with the asset allocation mentioned, and in particular, the relatively high allocation to Australian shares

- Have a very high risk tolerance.

See this article for an in-depth explanation of GHHF: GHHF – The moderately leveraged ETF

Summary of composition of all-in-one funds on the Australian market

| Vanguard | Betashares | ||||||

|---|---|---|---|---|---|---|---|

| VDCO | VDBA | VDGR | VDHG | VDAL | DHHF | GHHF | |

| Aus shares | 12% VAS | 20% VAS | 28% VAS | 36% VAS | 40% VAS | 37% A200 | 37% A200 |

| Int shares (unhedged) |

8.5% VGS

2.0% VISM 2.0% VGE |

14.5% VGS

3.5% VISM 3.0% VGE |

20.5% VGS

5.0% VISM 4.0% VGE |

26.5% VGS

6.5% VISM 5.0% VGE |

29.5% VGS

7.0% VISM 5.5% VGE |

VTI [1]

SPDW [1] SPEM [1] |

BGBL [2]

BEMG [2] |

| Int. shares AUD-hedged |

5.5% VGAD | 9 VGAD | 12.5% VGAD | 16% VGAD | 18% VGAD | — | 19% HGBL |

| Fixed income |

18% VAF

42% VBND 10% Cash |

15% VAF

35% VBND |

9% VAF

21% VBND |

3% VAF

7% VBND |

— | — | — |

[2] 44% total – ratios float with market capitalisation

Final thoughts on choosing an all-in-one or roll your own

By now, you should understand the pros and cons, but here’s a summary:

All-in-one diversified funds

- Simplicity and ease

- No need to rebalance

- Removes behavioural risk of tinkering

- Enables your partner to manage finances when you’re unable to

DIY

- Cheaper

- Ability to customise

- More tax-efficient

It’s going to be difficult to beat all-in-one diversified funds, so it is still an excellent choice despite some downsides. For those who want a little more control, you can go the DIY option – it’s not that much more work in practice if that’s what you prefer.

If you’re still unsure, I have two suggestions to consider.

- Focus on the big items in the pros and cons list

- The most significant item for many will be removing the behavioural risk of seeing something in the news and then selling down your assets after the entire market (who has access to the same news) has already reacted. Then you buy after it has gone back up. If you’re the type to tinker, going with an all-in-one outweighs all the cons combined.

- If you have an iron will and that is not a problem, then the ability to customise is probably the next biggest point to consider.

For example, if you already have investment property, it makes the most sense for your portfolio’s equities portion to be entirely global (unhedged).

Another example might be that you’re able to save enough for retirement without facing additional risks to meet your goals, and therefore have no need to take more concentration risk to chase franking credits and prefer to go with an all-global portfolio.

- Strive for simplicity

- If you still have no opinion one way or the other, consider the simpler approach of fewer funds. It doesn’t make sense to make things more complicated without a reason.

—

Thank you to Zennon (for the infinitieth time), Oz-FI, and Yen for the excellent input.